A company I advised ran aggressive outbound for eighteen months. Pipeline grew, but CAC stayed flat. The board questioned the spend at every quarterly review. Then something shifted. Organic inbound started contributing: first 5% of pipeline, then 12%, then 20%. Win rates on inbound deals were double outbound. Sales cycles were 40% shorter. The blended CAC started declining for the first time.

The CEO called me after the third quarter of improvement. “When did this happen?” It didn’t happen at a point. It happened over a period. But there was a moment when the curve changed. The mass they’d built through eighteen months of consistent market presence was generating its own gravity. They’d crossed an inflection point.

The question every growth-stage company faces is whether they’re approaching that moment, past it, or nowhere near it. Get the answer wrong in either direction and the consequences are severe.

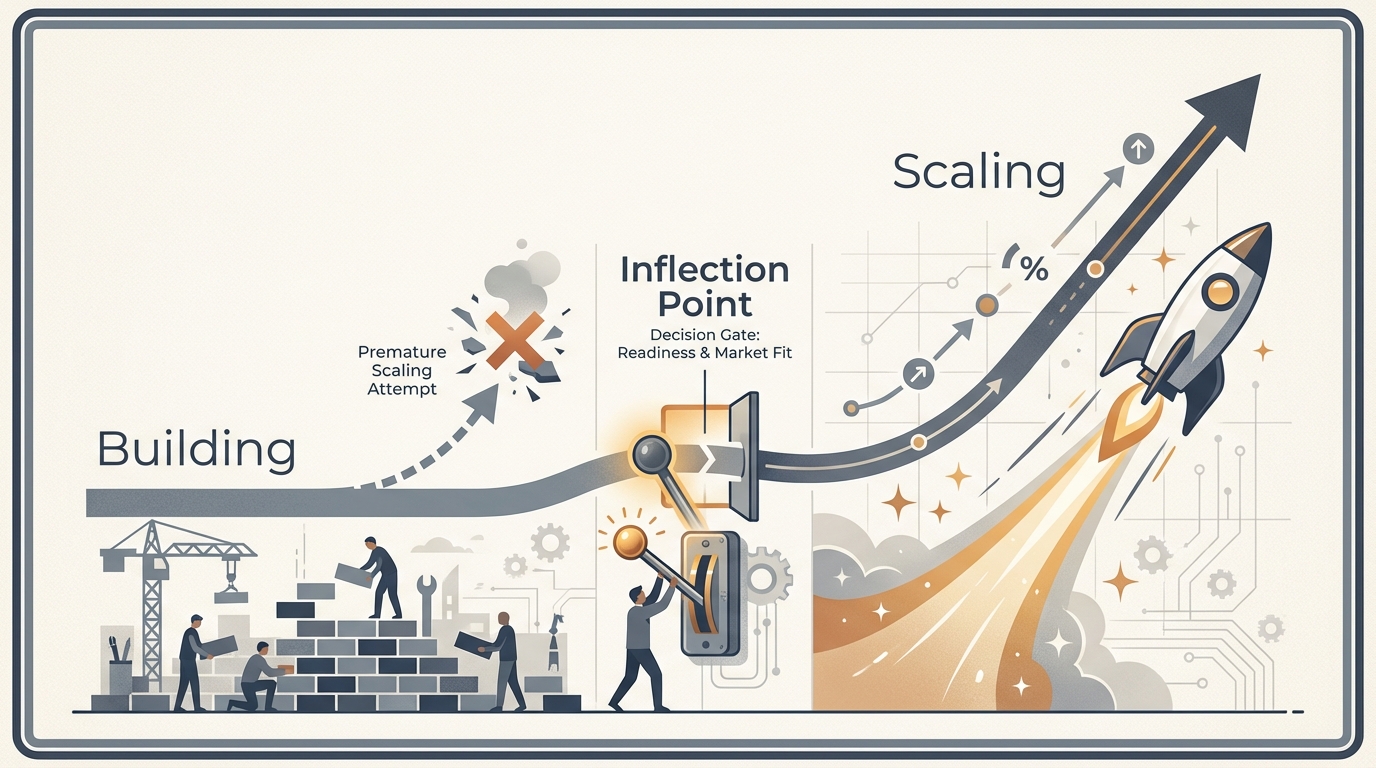

What an Inflection Point Actually Is

In mathematics, an inflection point is where a curve changes from concave to convex. The rate of change itself changes. In a growth system, it’s the moment when incremental investment starts yielding exponential returns. Before it, you’re building. After it, you’re scaling. The entire question of growth timing reduces to whether you’ve crossed this threshold.

This is one of six forces in the Coherence Model framework, and it interacts with all of them. Inflection points don’t emerge from nothing. They’re the product of accumulated mass (market presence, brand authority, content depth) reaching a critical density where the system starts to compound. You cannot will an inflection point into existence by spending harder. You can only build the conditions that make one possible, and then recognize it when it arrives.

The recognition problem is real. Inflection points don’t announce themselves. They leave clues: conversion rates stabilize above target, CAC payback period hits acceptable range, win rates against specific competitors improve, sales cycle duration decreases, the inbound-to-outbound ratio shifts. The key word is consistent. One good quarter isn’t an inflection point. Three quarters of improving metrics on steady investment might be. The companies that identify inflection points early are the ones tracking leading indicators (conversion trends, win rate trajectories, organic-to-paid ratio over time) rather than lagging ones (total pipeline, revenue, bookings).

The Two Failure Modes

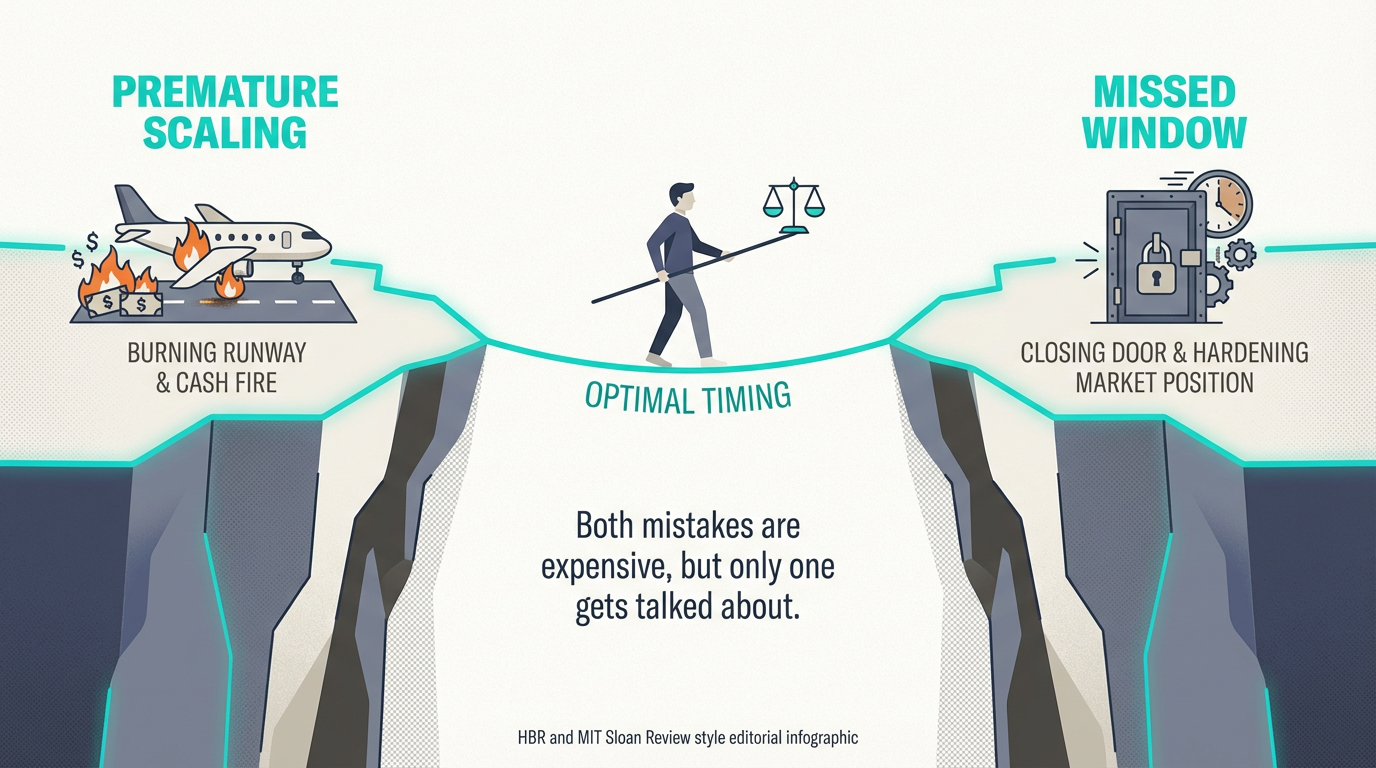

Most companies get the timing wrong. The failure modes are symmetric but not equally common, and understanding both is the only way to calibrate the decision.

Premature scaling is the more frequent mistake, and the pattern is predictable enough to be its own case study. Company raises a round. Board sets aggressive growth targets. Leadership hires ahead of demand and increases growth spend 3-5x. Efficiency collapses because the system doesn’t have enough mass to absorb the force. CAC spikes. The pipeline that looked promising at lower spend doesn’t scale linearly. Within two to three quarters, the company cuts back, retrenches, and restarts, having burned six to twelve months of runway proving what the physics would have predicted: velocity without mass is a treadmill.

This happens because external pressure, from investors, boards, and compensation structures tied to growth targets, pushes for scale before the engine can support it. The GTM leader churn pattern is often a direct consequence. Leadership gets replaced for “missing targets” when the real problem is that the targets assumed an inflection that hadn’t occurred.

Scaling too late is less common but potentially more damaging. It happens when leadership is traumatized from previous premature scaling and overcompensates with conservatism. Or when finance maintains tight spend limits past the point where the data supports expansion. Or when the team mistakes efficiency at small scale for readiness to stay at small scale, confusing discipline with stasis.

Missing the window matters because markets consolidate. Category positions harden. Buyers make decisions about who the default vendor is, and increasingly, AI systems encode those decisions into recommendations that become self-reinforcing. A company that reaches escape velocity while you’re running a careful pilot is a company you may never catch. The cost of moving too late doesn’t show up as a line item. It shows up as a market position you never occupy.

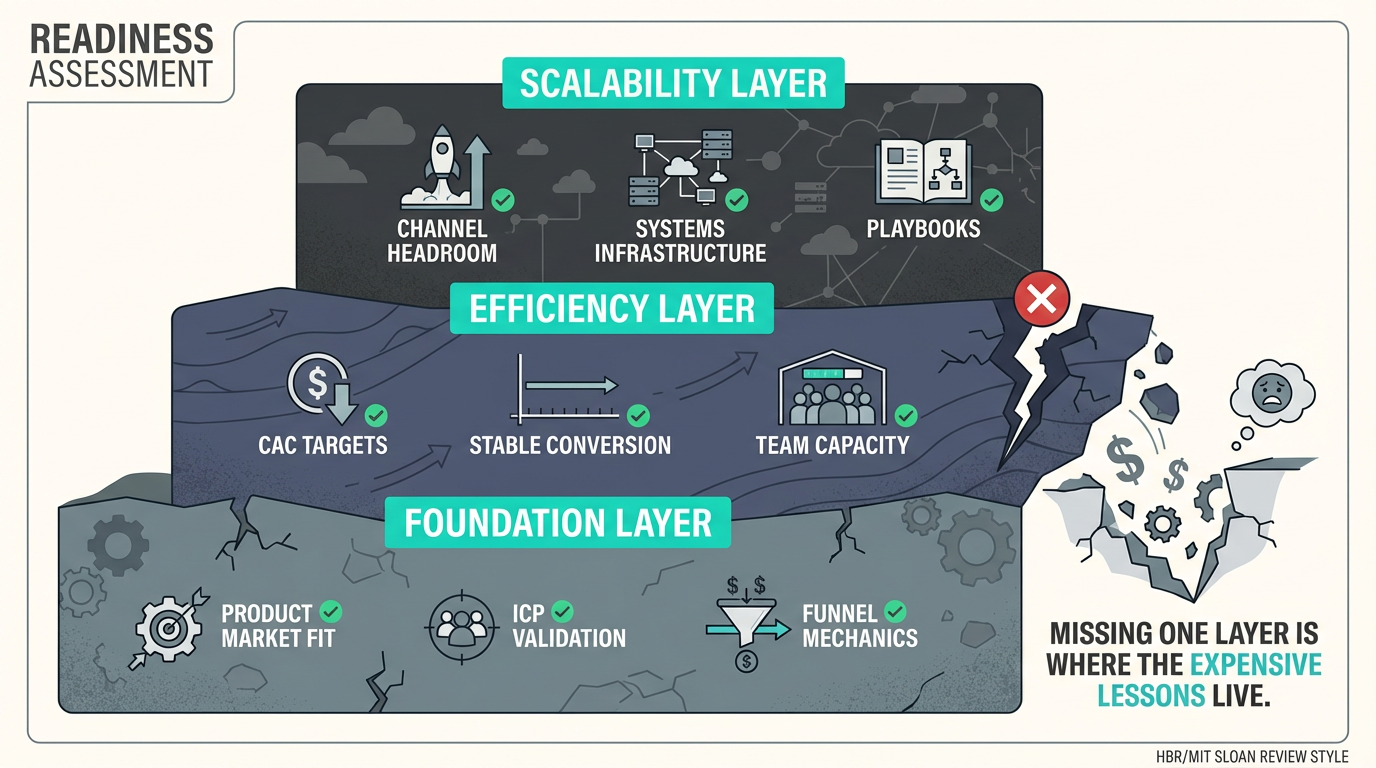

Reading the System

I think about inflection point readiness in three layers. All three need to be present before scaling makes sense. Missing one is where the expensive lessons live.

The foundation layer is whether the basics are proven, not assumed. Product-market fit is validated through retention and expansion, not through the founder’s conviction. The ICP is defined through closed-won analysis, not through the slide deck from the Series A pitch. Basic funnel mechanics work: you can trace the path from first touch to closed deal and the conversion assumptions at each stage are internally consistent. Unit economics make sense at current scale, not in a model that requires 10x volume to break even.

The efficiency layer is whether the system performs well enough to survive acceleration. CAC is at or below target. Conversion rates are stable, not improving because you’re cherry-picking deals. Sales can handle current volume without heroics. Customer success isn’t drowning in onboarding debt. If any of these are strained at current scale, adding 3x the volume won’t fix them. It will break them.

The scalability layer is whether the infrastructure can absorb growth. Channels have headroom: if you’re already spending to the point of diminishing returns on your primary channel, scaling means finding new channels, which is a different and harder problem than increasing spend on proven ones. The team can absorb growth without requiring a six-month hiring cycle first. Systems (CRM, marketing automation, billing, onboarding) can handle 3x volume without manual workarounds. Playbooks exist so that new hires can execute the motion, not just the people who invented it.

Making the Call

When the three layers check out and the leading indicators show consistent improvement, you have a decision. Not a formula. A decision.

The conservative path is to increase spend 50-100%, validate that efficiency holds at the new level, and scale further once you have proof. This is the lower-risk approach, and for companies with limited runway or in stable markets, it’s often the right one. The downside is speed. If a competitor is also approaching their inflection point, the conservative path cedes first-mover advantage.

The aggressive path is to increase spend 200-300%, accept that efficiency will dip temporarily as the system adjusts, and bet on capturing market position before the window closes. This requires more capital, more organizational resilience, and a genuine belief that the inflection is real and not a blip. The downside is obvious: if you’re wrong about the inflection, you’ve accelerated into a wall.

The right choice depends on the competitive dynamics (is the window closing?), the capital position (can you sustain the bet if efficiency takes two quarters to recover?), the team’s capacity to execute at higher velocity, and the market timing. None of these are knowable with certainty, which is why this is a decision and not a calculation.

What the Physics Say

The interaction between inflection points and the other forces in the framework is what makes the timing decision clearer than it seems in isolation.

Before the inflection, the priority is building mass and reducing friction. Investment should go toward accumulated market presence (brand, content, positioning, credibility) and removing unnecessary resistance from the buyer journey. The metrics that matter at this stage are mass indicators and efficiency ratios, not pipeline volume.

After the inflection, the priority shifts to increasing velocity and expanding surface area. Momentum is now the north star. The programs you built during the mass phase start compounding, and the question becomes how fast you can feed the engine without breaking the system that makes it work. The metrics shift too: now you’re watching blended CAC trajectory, organic-to-paid ratio, and whether efficiency holds as spend scales.

The companies that time it right are the ones that resist the pressure to scale before the physics support it, and then move decisively when the data says the system has changed. The gap between “we think we’re ready” and “the system is actually ready” is where most of the expensive mistakes live.

Nick Talbert transforms how B2B companies go to market. As founder of Strategnik, he helps founders and revenue leaders turn scattered tools and teams into pipeline, conversion, and growth that compounds.